Blog

Unpacking the Canada Performing Arts Workers Resilience Fund (CPAWRF)

Uncover all of the free and paid learning opportunities, supported by the Department of Canadian Heritage, as well as the four emergency support funds offered to artists in the performance sector.

So many free or PAID learning opportunities to take advantage of before March 31st!

Here at Generator, we love learning!

In October, the Department of Canadian Heritage announced 59 new projects for self-employed cultural workers in the live-performing sector (under the umbrella name Canada Performing Arts Workers Resilience Fund or CPAWRF). This program is the second half of the multi-million dollar investment in the pandemic recovery for the performing arts sector. Before we dive into some of the programs available now, we want to make sure you know about the Emergency Support programs that were launched this past summer.

The Emergency Support Program opened four (4) funds. For performing arts workers in Quebec, the fund is managed by La Fondation des artistes, and the remaining three (3) funds are for the rest of Canada. The Reactivation Program (managed by the AFC), the Resilience Fund (for dancers, managed by Canadian Dance Assembly) and the Live Music Workers Fund (for musicians, managed by Unison) are each offering $2,500 in direct financial support to help restore and reactivate your work. Note you can only apply to one of these four (4) funds.

In particular, the Reactivation Program is for folks who are underemployed OR have more than enough work right now BUT incurred debt or drew down savings during the pandemic - we are sure this is you! You must be able to show that you worked in the performing arts within the past 5 years. For more information about eligibility, head over here.

Now, back to the 59 new projects, we have compiled a database (which is growing as programs are launched) to make it easy for you to find out what is out there. Now go and learn for a fee or for free!

*Note all programs are offered in English and French. This database will focus on opportunities focused on a national and/or Ontario constituency.

If we are missing a program or you would like a program entry changed, please email kristina@generatorto.com.

The HST Dilemma

You’re in one province, the person who hired you is in another. You’re Zooming sixty unknown faces, and you have no idea which province any of them lives in. How do you know which sales tax rate to charge in the working-from-home era?

A big question that arises for folks who collect GST/HST comes down to invoicing: when you do charge GST? Or is it supposed to be HST? Why do I have a customer asking me not to charge sales tax?

(Looking for a general discussion of GST and HST? Like…when and how you’re supposed to register to collect it? Check out the GST and HST page on ArtistProducerResource.com.)

Place of Supply

This can be a funny rule to wrap your head around—made even more complicated by the fact that we’re now all working in the digital world, with many clients and customers farther away from us than ever before (while we ourselves stay closer to home than ever before...three cheers for #PandemicLife).

CRA uses the term “place of supply” when determining which rate of sales tax to charge. This means that you charge the GST or HST rate based on the location where you are supplying your product or service. So you may be handcrafting that macramé in your basement suite in Toronto, or hosting that Zoom consultation from your home office in Vancouver, but what counts is where your product or service is being consumed.

An easier way to think of it is: where are you sending your invoice (i.e. what is the business address of the person who’s paying you)? If you’re invoicing a company located in Quebec, you charge the 5% GST in place in that province. Sending your product to a customer in New Brunswick? You charge them New Brunswick’s 15% harmonized sales tax. (See below for a table of which rates to charge in what province.) If you have an out-of-province client telling you not to include sales tax on your invoice, they’ve got that wrong: if you are registered to collect GST/HST, you need to do so, you just need to insure you’re charging the correct rate according to the province of supply. As detailed in the table below, the only instance in which you would not charge sales tax is if you’re invoicing internationally.

A helpful way to understand the “place of supply” rule is to think back to that fabled time when we could all gather together. (You know, back when we used to physically go places to experience a performance?) If an Alberta resident purchased a ticket to see a play at Tarragon Theatre, they’d pay 13% HST on that ticket because Tarragon is located in Ontario—not 5% because the person purchasing the ticket is visiting from Alberta.

The Complicating Factor

What makes things tricky in the online world is that now, thanks to *official pandemic sponsor* Zoom, we’re able to host events and invite people into our space—whether it’s for online classes, workshops, or performances—and those people could be consuming what we’re offering from pretty much any location. You’re unlikely to be gathering your meeting guests’ mailing addresses and sending them individual invoices, so in this kind of scenario, CRA states that you would charge the sales tax rate of where you are located. However, if you are hosting a one-on-one session with someone, like a vocal lesson, you would charge sales tax based on the location of that individual (e.g. if you’re based in Newfoundland and offering a vocal lesson to someone in Toronto over Zoom, you charge Ontario’s 13% HST).

The first question to ask yourself is whether you’re sending an invoice for your service or product—and if you are, easy, just follow the Place of Supply rules. For example, if a company in Manitoba is paying you to host a workshop for 50 people on Zoom who could be tuning in from wherever, you charge Manitoba’s 5% GST—you are getting paid by one person/company whose business address is in Manitoba (rather than getting paid individually by workshop registrants), and that trumps the fact that the Zoom participants are located from all over.

For more information and examples from the CRA, check out:

GST/HST Rates Across Canada

The rate for taxable supplies depends on the province or territory. As of February 10, 2021, the rates are:

Got Questions?

If you are a performing artist working in Canada and have further questions, please contact us by emailing info@generatorto.com and we will consult with you at our next Financial Joy Office Hours session. Please note that at this time we are not able to offer support to folks working outside the performing arts.

Learning Pathway: Tax Season

For our second ArtistProducerResource.com Learning Pathway, Financial Literacy Consultant Audrey Quinn offers a step-by-step approach to tackling the most wonderful time of the year…tax season.

For our second ArtistProducerResource.com Learning Pathway, we’re ringing in the most *wonderful* time of the year! The time of year when you’re looking through pockets, drawers, and in between couch cushions for receipts. When you’re trying to figure out what that deposit in your bank account back in June was from. When you’re wondering if that dinner you went to with that touring company last January is deductible. Yes: it’s tax time. Maybe you started 2020 with the best of intentions, swore you’d stay on top of your finances all year long, but then life happened (and a certain pandemic happened, too). So now you’re sitting in front of a pile of papers faced with what feels like one very complicated tax return.

One Step At A Time

Step 1

Don’t fret. It may seem overwhelming at first, but if you take a systematic approach and break tax prep into smaller steps, it will feel more manageable.

Step 2

Familiarize yourself with the Canadian tax system and your obligations as a tax payer by reviewing the Income Tax page on ArtistProducerResource.com.

Step 3

Identify all the income you earned during the tax year (in this case, January 1, 2020-December 31, 2020). This may mean gathering together invoices you sent out, service contracts you signed, and records of deposits. You will also have to report any income that was reported to CRA in the form of T4s, T4As, T3s or T5s. By February 28, you should be able to see all applicable forms issued to you via CRA MyAccount.

Step 4

Organize all expenses related to your self-employment by type of expense—think office supplies, union dues, agent fees, home office materials, business meals, etc.

Step 5

Don’t forget about tax deductions that are available to all Canadians, regardless of self-employment status. (These include Medical, Donations, RRSP Contributions, Ontario rent credits.)

Step 6

If you’re feeling confident, you can prepare your tax returns using any CRA-approved tax filing software, or you can book an appointment with a tax professional. Make sure you’re up front when booking a tax appointment that you are a self-employed artist and that the tax preparer is familiar with your line of work. Not all tax preparers are created equal and it’s up to you to advocate for your needs.

Step 7

If you’ve decided to have your taxes done by a tax professional, be sure to review Artbooks’ “Prepare to Meet your Tax Preparer” guide before your appointment to make sure you have everything you need to make that session run smoothly.

Things to Consider

Grant Income

One aspect of personal income tax that is unique to artists is the receipt of grants. Grants are a welcome source of revenue for artists but can create quite a tax headache. Our Guide to Government Grants and Their Tax Treatments will help you with preparing your taxes after receiving a grant.

Employment Status

Unsure whether you should be (or might want to be) considered an employee rather than a contractor, or vice versa? Visit Employee vs. Contractor on ArtistProducerResource.com to learn the differences between the two (there are pros, cons, and tax implications for each).

Planning Ahead

Once you’ve climbed the tax prep mountain and emerged on the other side, it might be a good time to double down on a commitment to get/stay on top of your finances going forward. This will help you feel less overwhelmed next tax season, and will help avoid any nasty surprises—tax bills can be scary if you’re not prepared for them.

We recommend you take a hard look at your finances and plan a budget for yourself by checking out the tools and templates for Personal Finances and Planning on ArtistProducerResource.com. You might also be inspired to revamp your invoice template (which can be found on the Income Tax page) to make next tax season that much more bearable.

Keep Learning

Congratulations on wading into the murky waters of taxes as an independent artist. Your financial learning may have taken the backseat to your artistic learning in years past, but there’s no time like the present—we’re glad to see you here now! And remember, you’re not alone, and there’s lots of help around. There are plenty of further learning and development opportunities to help you with budgeting and personal finance. Some of our favourites are: Rags to Reasonable, Ambitious Adulting, and The New School of Finance.

About ArtistProducerResource.com

ArtistProducerResource.com is a free, searchable online encyclopedia of information, resources, tools, and templates for producing independent performance work in Canada, currently with a focus on Toronto. Launched in November 2017, it has since been visited by over 10,000 users, transforming the way artists producers access information and share knowledge across Canada. ArtistProduceResource.com is free to access and always will be. You can become a supporter by subscribing to our Patreon—we’ll send you a monthly newsletter with highlights, features, and all the newest content on the site. Got a suggestion for ArtistProducerResource.com? Send it to us here.

Resource Round-up: Financial Literacy

A collection of our favourite financial resources. Explore categories for artists, producers and non-profit workers, and tax season.

We’ve pulled together the best of ArtistProducerResource.com, our blog, and our favourite external resources to help you navigate finances as an artist, producer, nonprofit worker, and/or human who wants to be ready for tax season for once.

These resources will also be available via Toronto Fringe’s Next Stage Community Booster Self-Care Hub (access is pay-what-you-can) from January 21-31, 2021.

From CERB to CRB

The CERB program, which has allowed eligible Canadians to collect $500/month since March 15, ends September 27 and is transitioning into two programs.

[Last updated: October 16, 2020] We don’t need to tell you how long it’s been since the pandemic was declared - we all know that. We’re here to help clarify updates to the government benefit programs, which we’ve written about in previous blog posts (March 18, March 20, and July 8).

The CERB program, which has allowed eligible Canadians to collect $500/month since March 15, ends September 27 and is transitioning into two programs.

EI

The first of those programs is for Canadians who are eligible for EI (meaning: you worked at a job where taxes were deducted at source). Traditionally, EI benefits are based on how many hours you worked in the past year, how much you were paid and what the unemployment rate is in your region. CRA is making it easier for Canadians to qualify for the benefits and guarantee them a minimum benefit rate. The support comes in three ways:

This is what you’ll see if you head to Service Canada to apply for EI benefits.

One-time insurable hours credit. Canadians who lost their job will get a credit of 300 hours (or 480 hours if you had to leave your job to care for sick family members or were sick yourself).

A base unemployment rate of 13.1% across Canada. Traditionally, regional unemployment rates are used to calculate the number of qualifying hours and length of time you can access the benefits. By setting a base unemployment rate, that makes the number of qualifying hours 420 and a minimum entitlement of 26 weeks of benefits.

Minimum benefit rate. The government has guaranteed a minimum weekly rate of $500 regardless of how much you earned from your previous job.

For those that qualify for EI – you can apply for these benefits through Service Canada, as you would have under “normal” circumstances.

CRB

The next program is for freelance/gig/self-employed workers who wouldn’t qualify for EI (because you didn’t work at a job where taxes were deducted at source). This new program is called CRB (Canada Recovery Benefit).

The CRB goes into effect September 27 and will last for one whole year. It consists of weekly payments of $500 for a maximum of 26 weeks (read: even though it will run for the full year, the maximum you can receive the benefit is for 6 months total within that year).

It has the same qualification requirements as CERB. You must:

Be over 15 years old

Have lost your job (not quit)

Not be eligible for EI

Have stopped working due to COVID and be available and looking for work

Have had income of at least $5,000 in 2019

Have experienced at least 50% reduction in weekly income

Eligible Canadians will need to apply for the benefit for every two-week period.

There are four things to note with regards to this benefit:

If your net income (income less deductible expenses) is more than $38,000 at the end of the year, you will need to repay a portion of the CRB benefit. You would need to repay $0.50 for every dollar above $38,000. For example, if you collected CRB for 10 weeks for a total of $4,000, and your net income at the end of the year is $39,000, you would have to pay back $500 of the CRB. CRB (and CERB) payments are both taxable so they would be included in your annual net income.

How do you know if your weekly income has dropped by more than 50%? This is obviously confusing for self-employed people who don’t earn a regular weekly salary. But the government has offered some guidance to try and help: If you are applying for CRB in 2020, you will compare your income to your average weekly income in 2019. So, you take your total income from 2019 tax return (in majority of cases it will be box 15000 on page 3 of your tax return, or to be more specific the total of boxes 10100, 10400, 135000, 137000 and 139000 - see this PDF for reference), and divide it by 52. Then compare it to the weekly income in the current year’s eligibility period to see if the drop is more than 50%.

For example: Say your total income from 2019 was $52,000. Your average weekly income would be $520 and your bi-weekly average income would be $1,040 ($520x2). If you earned less than $520 TOTAL ($1,040 / 2) in the 2- week period you’re applying for, you would qualify.Scenario A: You get paid $500 for a writing job that takes you two days to work on and those are the only two days you worked in that 2-week period - you would qualify.

Scenario B: You get a consulting gig that pays you $1,000 for 10 days of work. If those 10 days are all within the two-week period you’re applying for, then your income for that period is too high and you don’t qualify for that period. But if those 10 days of work are spread out over a full month, and only two of the days you work on the writing gig are within this particular eligibility period, your income earned in that period is only $200 ($100/day x 2 days) and you would qualify. This goes back to what was discussed in a previous post about earned revenue and timing. It doesn’t matter which day you received the cash, the income CRA is referring to in this eligibility requirement is when you earned it (or when you did the actual work for it).

Taxes will be withheld from CRB payments. This means that for every two-week eligible period, you will receive $900 in your bank account. $100 will go towards your tax payment at the end of the year. Which is a good thing, because these payments are taxable at the end of the year anyway!

Application periods are retroactive. For CERB you applied for the two-week period in advance, but for CRB you are applying AFTER the two-week period. This means that the earliest you can apply for the first two-week period (Sept 27 – Oct 11) is October 12. For this first period, you must attest that you were looking and available for work and didn’t earn more than 50% of your 2019 average weekly income in either week from Sept 27 – Oct 4 or Oct 5 – 11.

Updated October 8: the CRA has added a CRB Q+A on their website—find it here.

Updated October 13: Derrick Chua created a wonderful document to help you navigate these calculations.

Be Prepared for 2020 Taxes

So, now is a great time to get a head start on your 2020 taxes! (Accountants everywhere cheer, you groan). We highly recommend that you begin gathering the invoices and income collected in 2020 and keep a tracking chart to see how much you have earned so far. At the end of the year you will have deductible expenses that will reduce that overall income, but if you know the income earned (aka – gross income) you will at least know the maximum amount of income you will report for 2020. If your gross income is over $50,000, you’ll probably end up with a net income (gross income after deductible business expenses) higher than $38,000 and will have to pay back the CRB.

Got Questions?

We understand that every individual situation is unique and this post can’t address the needs of everyone – if you are a performing artist working in Canada and have further questions, please contact us by emailing Lead Producer Kristina Lemieux (kristina@generatorto.com) and we will consult with you at our next Financial Joy Office Hours session. Please note that at this time we are not able to offer support to folks working outside the performing arts.

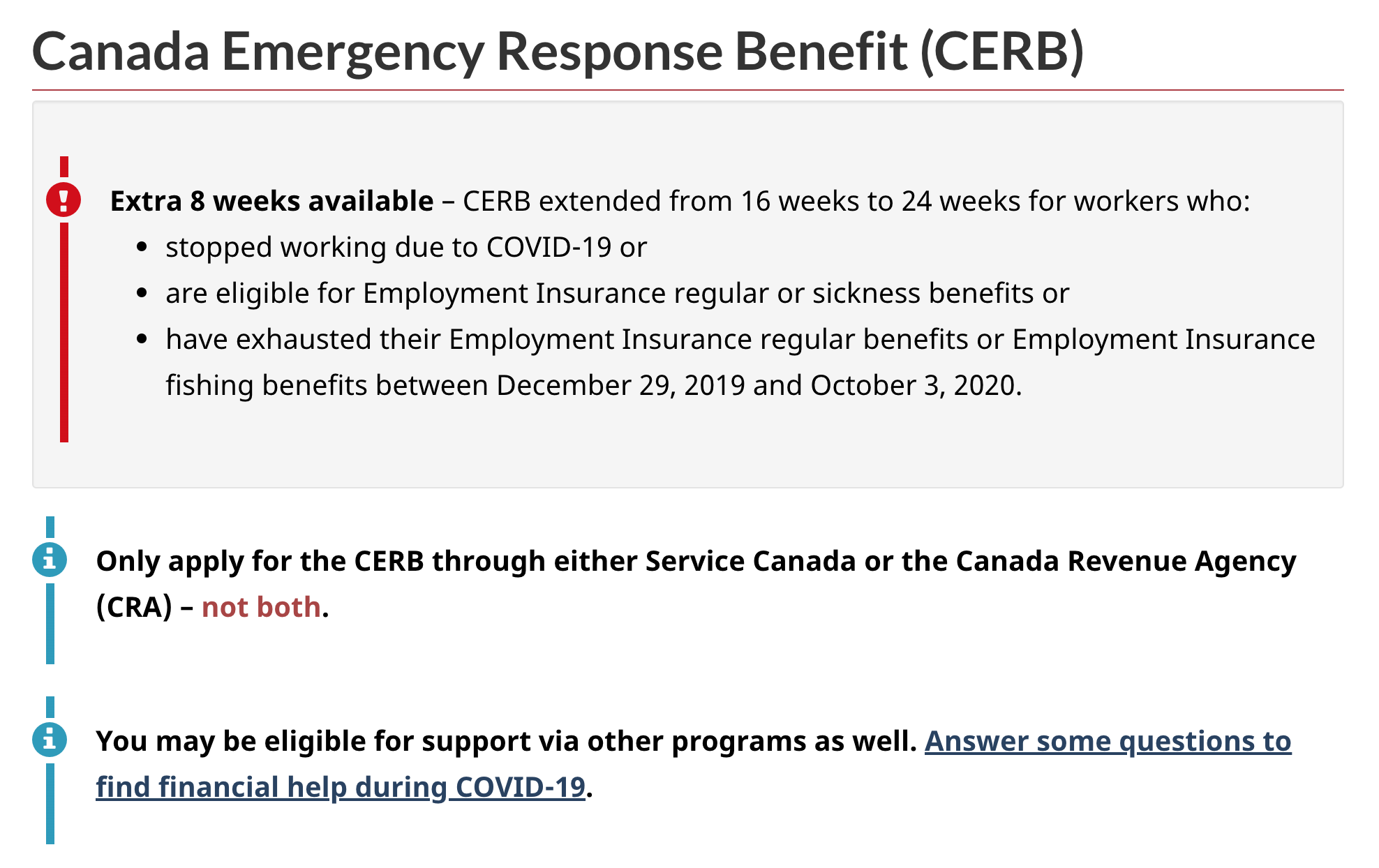

An Update on CERB

CERB has been extended another eight weeks to August 29 (a change from a 16-week eligibility period to 24). Most of the same requirements apply as with the previous periods, with one notable addition.

A screenshot from the Government of Canada website captured on July 8, 2020. Alerts remind site visitors that the CERB has been extended from 16 to 24 weeks; that applications to the CERB can be made via the CRA or Service Canada (but not both); and that anyone eligible for the CERB may be eligible for support via other programs as well.

[Last updated: July 8, 2020] It has been three months since the government introduced the CERB payments, and although we were all hopeful that businesses would be back to ‘normal’ by now, that has proved to be far from the truth. As some businesses begin to reopen, many artists are still waiting to see their sources of income come back.

CERB Extension (and one change)

CERB has been extended another eight weeks to August 29 (a change from a 16-week eligibility period to 24). Most of the same requirements apply as with the previous periods, with one notable addition. Recipients must now sign an attestation stating that they are actively looking for work. This is an ordinary requirement for people collecting unemployment insurance, and since CERB is acting as a parallel for unemployment insurance, this additional requirement makes sense.

Eligibility

As a reminder, CERB is available to those who:

Are over the age of 15 and living in Canada

Have stopped working because of COVID (either because they were sick, taking care of a sick person, or taking care of children who can’t get daycare)

Earned at least $5,000 in the last 12 months (before self-employment deductions)

Have NOT quit their job voluntarily

Have NOT earned more than $1,000 in the period in which they are claiming the benefit

The CRA has not released any information on how they will be confirming recipients’ eligibilities. At the moment, it is up to the individual to attest to their own eligibility.

Timing of Earnings

One question that has come up often with respect to self-employed artists is the timing of that $1,000 earnings restriction. We have heard from many people who are nervous about depositing a cheque into their bank account because they are worried it will alert the CRA that they have earned that income at that time. However, the revenue restriction is based on the timing of when you earned it, not when you physically received the money. If you worked on a project in January and the client has just paid you now, that payment does not count towards the $1,000 earned income for the period in which you’re depositing that money into your bank account. It was earned back in January, not today. Keep in mind, the reverse is also true: if you’re doing work on a paid project now, you’re technically earning that money now – even if you don’t get paid for it until October.

The same would apply for royalty payments. If the royalties are earned for work you did during the application period, that would count towards the $1,000 minimum, but not if the royalties were for work you completed in a prior period.

The CERB government website is actually quite helpful and lists a number of scenarios to help you understand when and if you qualify for the benefit.

Note

[July 20, 2020] We’ve been hearing that folks are getting conflicting information about time of earnings v. time of payment, so we want to clarify how we arrived at the above conclusion. Under the accrual basis of accounting, revenues are reported on the income statement when they are earned. When the revenues are earned but cash is not received, the asset will be recorded as accounts receivable. In contrast, under the cash basis of accounting, revenues are not reported on the income statement until the cash is received. (Source: AccountingCoach.com)

CRA is making no distinction between accrual or cash accounting - but generally accepted accounting principals use the accrual method. One valuable reference point here is the question and answer below, via the government CERB website:

“Do artists’ royalties count as employment or self-employment income with respect to the CERB?

”Yes, in some cases. Artists’ royalties would be considered payments received as self-employment income if they were received as compensation for using or allowing the use of a copyright, patent, trademark, formula or secret process that is a result of their own work or invention. These royalties count towards the $5,000 income threshold, as well as towards the $1,000 that claimants can earn per month while receiving the Benefit. However, royalty payments received from work that took place before the period for which a person applies for the Canada Emergency Response Benefit do not count as income during that specific benefit period. Other royalties (i.e., from investment activities) do not count with respect to the Benefit.”

Retroactive Applications

Keep in mind that applications to CERB can be made retroactively, up until December 2, 2020. So if you didn’t apply because you didn’t think you qualified, but when you reviewed the eligibility requirements you in fact were eligible – you can apply at any time before December 2.

More Resources

Rags to Reasonable’s Chris Enns shared ‘9 Thoughts on Financial Planning in the Time of Covid.’

This is the third post in our blog series on Artist Finances in the Time of Covid. If you’re looking for more context, check out The Economics of Covid-19 for Arts Workers and Tracking Financial Losses due to Covid-19, both of which were last updated on March 30, 2020.

If you are in crisis, here are some resources on ArtistProducerResource.com: Mental Health, Health Care, Housing and Childcare, COVID-19 Artist Health & Safety

The Economics of COVID-19 for Individual Arts Workers

The “Canada Emergency Response Benefit” was announced on Wednesday, March 26 - and it already has a fun acronym.

Please note this post has not been updated since March 30, 2020 and should not be referred to for the most up-to-date information.

Updated on March 30, 2020. Can you believe it’s only been a week? So much has changed! And they just keep changing.

Tax Deadlines

Registered Charities

The filing deadline for registered charities has been extended to December 31, 2020 for any charities with T3010s due on or after March 18. In normal life, T3010s are due six months after the charity’s year-end. So this extension means that for any charities with year-ends between September 18 and June 30 now have until December 31, 2020 to file their T3010s.

Individuals

The tax deadline for individuals has been moved from April 30 to June 1. Currently, the June 15 filing deadline for self-employed individuals has not been changed.

Tax payments are now due August 31 (instead of April 30).

We still recommend preparing your taxes as soon as possible, so that you know what balance you’re working with - plus, if you qualify for a refund, it might be helpful to you to receive it sooner rather than later!

GST/HST Filing

Updated on April 1, 2020: Any GST/HST payments due between March 15 and May 31, 2020 are now not due until June 30, 2020. (The payments you choose to defer will all be due on June 30, 2020. ). The filing deadline has not changed, but there will be no penalties on late filing.

Read the government notice here.

Canada Emergency Response Benefit (CERB)

This benefit was announced on Wednesday, March 26 - and it already has a fun acronym. This is a combination of the “Emergency Care Benefit” and “Emergency Support Benefit” that was mentioned on the last edition of this blog post (points 1 and 2)…which we have conveniently removed so that you will no longer refer to them, as they are now irrelevant.

Updated on April 1, 2020: Trudeau said today that direct payments could arrive within five days, mailed cheques within ten days.

Learn more on the Government of Canada website here.

Who is eligible for CERB?

Anyone who is either: sick with COVID, quarantined, taking care of children, taking care of a sick family member PLUS anyone not receiving a paycheque because their workplace has been closed. You are eligible if you are a contractor (AKA – self-employed, freelancer) or an employee.

Update: Prime Minister Trudeau confirmed on April 1, 2020 that if you've already applied through EI, you're all set up for CERB - you do not need to reapply for the CERB when the portal opens. If you’re already receiving EI benefits, you can continue to collect your EI benefits and if your benefits run out before October 3, you can apply for CERB as well.

How much is it?

Applicants will receive $2,000 a month for 4 months. That’s $8,000 total. And it’s available for Canadians who’ve had their work disrupted between March 15 and October 3, 2020.

When can you apply & get your money?

The portal to apply is set to open on April 6 with payments coming as soon as 10 days after.

Updated April 2, 2020: The CRA has identified days of the week corresponding to birth month to help service applicants without overloading the system, once applications are open.

Born January, February or March? Apply on Mondays, starting Monday, April 6.

April, May or June? Apply on Tuesdays, starting Tuesday, April 7.

July, August or September? Apply on Wednesdays, starting Wednesday, April 8.

October, November or December? Apply on Thursdays, starting Thursday, April 9.

Any month may apply on Fridays, Saturdays and Sundays.

What do I need to prepare?

Well, the government hasn’t yet released details on what documents or information you need to provide but one can assume you will need the following:

Up to date taxes (you should have filed up to 2018)

What income you’ve earned so far in 2020

How much income you anticipate losing or have already lost due to this ‘disruption’ (learn more about how to do this in our blog post: Tracking Financial Losses due to COVID-19)

Side note: we know it can be scary to face the numbers, but trust us, it will make you feel better once you can quantify the losses and know the numbers you’re working with so you can come up with an actionable plan.Get registered for CRA My Account! If you forgot your login or your security pin – good news – you can call CRA and request to reset your password. You will need to have a copy of your last tax return on hand to answer their security questions. It’s possible your taxes need to be up to date to create MyAccount for the first time. The number to call is: 1-800-959-8281, or you can watch CRA’s How to Register for MyAccount video here (or click the video link above).

Note: the following two sections have not been changed since March 20.

GST credit

The government is proposing (read: this needs to be approved by all parties first) an additional GST credit of up to $400 for singles or $600 for couples. Currently, the maximum GST credit is $451 and individuals with income of less than approximately $48,000 qualify for this credit. The lower your income, the higher the credit you receive.

Student loan interest

The government is also proposing to stop charging interest on student loan for six months.

Other credits are being made available to Indigenous communities, parents, seniors with RRIF withdrawals, the homeless and women and children escaping domestic violence.

More Resources

A great breakdown about programs announced last week, compiled by Dr. Jennifer Robson of Carleton University

Sara Clarke is breaking down government announcements as they roll in on her blog page Financial Information During COVID-19

The official CRA bulletin that our initial breakdown was based off of

A great explainer and guide on how to survive this financial emergency

The COVID-19 Health and Safety for Artists page on ArtistProducerResource.com includes emergency funding initiatives, mental health tools, digital sharing platforms, food bank information, and external resource lists

Take care out there and support one another.

Did we mention it’s time to get set up online with a CRA MyAccount (if you’re not already)?

Tracking Financial Losses due to COVID-19

While our governments and arts councils are still in the process of determining what financial support they will be able to provide to workers who have been affected by event cancellations and public closures, they have all stated the importance of documenting your financial losses.

Please note this post has not been updated since March 30, 2020 and should not be referred to for the most up-to-date information.

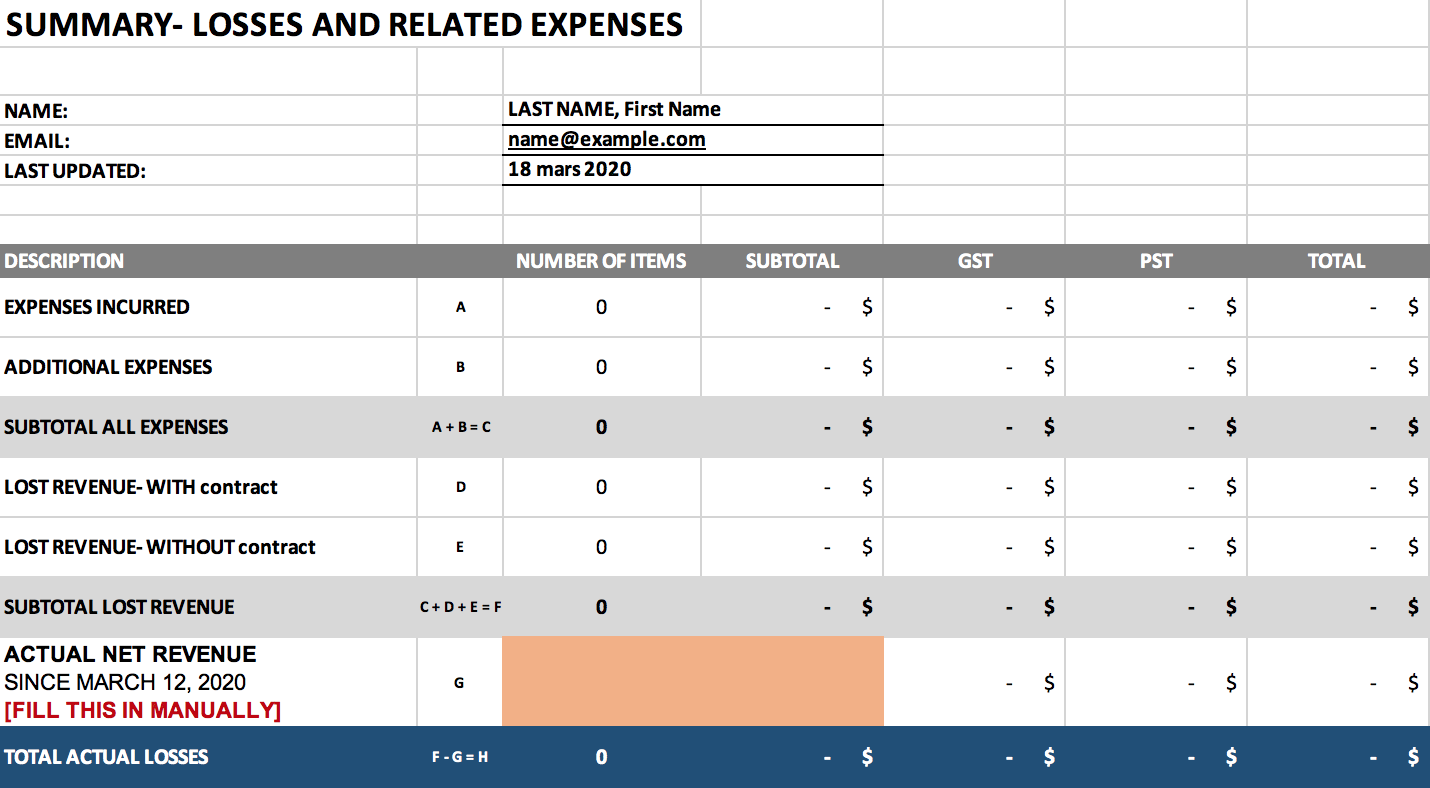

A screenshot from Arts Link New Brunswick’s Lost Income Tracking Tool.

What are your losses?

Those who work in the arts have been hugely impacted by physical distancing measures taken in response to the COVID-19 pandemic. While our governments and arts councils are still in the process of determining what financial support they will be able to provide to workers who have been affected by event cancellations and public closures, they have all stated the importance of documenting your financial losses. An important part of this is collecting all contracts and cancellation notices (that email you got notifying you that your show was not going on? Save it as a PDF).

Here’s what to keep in mind…

If you were producing an event that has been canceled or postponed, your financial losses would include:

Artist and production fees paid for the event that didn’t happen/hasn’t happened

Hours you have volunteered outside of the scope of your contract, likely due to making the decision to cancel/postpone and communicate it, as well as the time that goes into tracking your losses

Advertising (print or online) for the event and anything with dates on it that is no longer relevant, or that may become irrelevant should details change as a result of postponement (e.g. venue change, cast change)

Non-refundable deposits/payments for venue rental, equipment rental, etc.

Insurance

If you are postponing your event, it might be the right time to consider “remounting” costs, such as:

Additional Artist and production fees

Additional Producer fees

Advertising and rental costs

Rehearsal and Venue rental

Insurance

Potentially diminished box office revenues (given that future measures to ensure public health and safety may include lowered seating capacities and/or lower attendance)

It is very likely that these losses will need to be proven/documented, so make sure your invoices are well organized. If you didn’t have contracts, now’s the time to make them. If you are producing your own show, make an estimate of the time you already spent working on it, and will have to spend working on it in the future, and set a rate for yourself.

If you are wanting to track losses for work outside of the arts, such as in the service industry, it might be worth tracking the following things:

Hours worked each week for the past six months and, if relevant, tips earned - this will help estimate your losses related to the cancellation/closure

Any emails or notifications from your producer/employer of event cancellation/business closure

Services, health care, or self-care expenses that you continued to pay while you were experiencing income loss and didn’t have the resources to cover the costs

Expenses that you incurred because you were expecting to work but did not, such as costumes/materials purchased, travel expenses

Tools

ArtsLink New Brunswick has created a Lost Income Tracker. Visit their website to download the Excel template in English or French.

Tau S. Bui and Pam Tzeng have created French and English versions (respectively) of a similar tracking tool, which gives you the option to select your province and input tax information relevant to you. Excel en français ici, Google Sheet in English here.

Other things to keep in mind…

File your taxes

Perhaps the most important thing is to make sure your taxes are up to date. Even if you are behind a couple of years, take the time now to file. Loss calculations are often based on past earnings. If you need support with your taxes, the Income Tax page on ArtistProducerResource.com is a good place to start.

On March 18, the Federal Government announced that the individual filing due date for 2020 will be deferred to June 1, 2020. Read more here.

Fill out surveys about your losses

Arts organizations with mandates to advocate for the arts sector have been and will continue to collect data about losses to the arts sector and artists. These surveys help these organizations advocate to government on behalf of the whole sector. Please take a moment to share your information and experience with them.

Canada: PACT Survey

Ontario: TAPA Survey

BC: GVPTA Survey (includes a budgeting framework)

Statements from funders about COVID-19

Canada Council (updated March 16, 2020)

Ontario Arts Council (updated March 16, 2020)

Toronto Arts Council (updated March 16, 2020)

Government Support

In general, Employment Insurance is a program is for folks who are employed and have had their employment disrupted through no fault of their own.

Here is a resource for applying for EI from BC that outlines how to apply:

For those out of work due to self-quarantine. Do not have to be laid off by your employer to qualify, but must be able to say your employer or a medical professional asked that you stay home. You must be unable to work from home to qualify.

For those out of work due to workplace closure due to COVID-19. Must have worked a combined total of 700 hours in the last year if you worked in Vancouver. This is all your workplaces combined.

For those on quarantine that may finish their quarantine to find their workplace closed.

On March 18, the federal government announced a COVID-19 emergency response package:

For Canadians without paid sick leave (or similar workplace accommodation) who are sick, quarantined or forced to stay home to care for children, the Government is:

Waiving the one-week waiting period for those individuals in imposed quarantine that claim Employment Insurance (EI) sickness benefits. This temporary measure will be in effect as of March 15, 2020.

Waiving the requirement to provide a medical certificate to access EI sickness benefits.

Introducing the Emergency Care Benefit providing up to $900 bi-weekly, for up to 15 weeks. This flat-payment Benefit would be administered through the Canada Revenue Agency (CRA) and provide income support to:

Workers, including the self-employed, who are quarantined or sick with COVID-19 but do not qualify for EI sickness benefits.

Workers, including the self-employed, who are taking care of a family member who is sick with COVID-19, such as an elderly parent, but do not quality for EI sickness benefits.

Parents with children who require care or supervision due to school closures, and are unable to earn employment income, irrespective of whether they qualify for EI or not.

It might be worth considering Self-Employment Insurance, however it is worth noting that even if you applied now, you would not be eligible for benefits until 12 months after registration.

Further Resources

If you’re in BC, here’s a handy guide for applying to E.I.

If you are in financial crisis, here are some resources on ArtistProducerResource.com:

A Guide to Preparing Your Taxes After Receiving a Grant

There are many theories on how to deal with your grant when it comes to tax time, not all of which are helpful. The most important thing to remember is that grants awarded to individual artists are taxable income to the recipient.

Receiving a grant is usually considered a great event; an occasion to break out the champagne and reward yourself, a moment to reflect that a group of your peers deemed you worthy and part of the community. Grants keep art afloat in Canada, and should be a cause for celebration. Until it’s time to do your taxes, and then the world seems to fall apart and you curse the day you received that $7,000 from the Canada Council for the Arts.

There are many theories on how to deal with your grant when it comes to tax time, not all of which are helpful. The most important thing to remember is that grants awarded to individual artists are taxable income to the recipient. A T4A is issued to the recipient and reported to the Canada Revenue agency (CRA), who will expect that income to be reported.

Government Grants and Their Tax Treatments: A Guide to Preparing Your Taxes After Receiving a Grant was created by Tova Epp, with graphic design by Kinnon Elliott.